Concepts

The economics of food delivery platforms

Unlocking opportunity in crisis

In every crisis lies an opportunity!

Food and grocery delivery platforms certainly seem to think so in the age of coronavirus, as app downloads and orders take off with lockdowns and social distancing in place.

This issue of the newsletter looks at the economics of food delivery platforms. A quick overview:

- The economics of food delivery platforms

- Asian food delivery platforms have an unfair margin advantage

- Food delivery margins: A textbook case of ‘what’s good for the platform is bad for the ecosystem’

- The ‘Netflix playbook’ in food delivery

- How to win low margin games

The economics of food delivery platforms

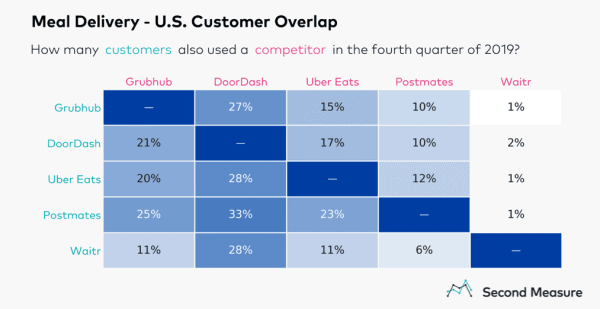

Much like ride-hailing, food delivery platforms have low multihoming costs, as I’ve explained before. All three stakeholders – diners, delivery agents, and restaurants can participate across multiple competing platforms. Across these, multihoming is arguably highest among diners.

The chart below reveals the extent of multihoming among the top players. (Source: SecondMeasure)

When looking at the health of a food delivery platform, you need to focus on two key metrics:

- Customer retention

- Peak customer spend i.e. maximum spend per customer per time period (per week or per month)

The higher the customer retention and the faster you can move a cohort of customers to peak customer spend, the more likely you are to make the unit economics work.

On the cost side, the marginal cost of delivery plays an important role. Food delivery platforms work with very thin margins per order. Hence, route optimization and number of orders per route are important criteria.

Delivery economics: An unfair advantage for Asian platforms

Given the importance of route optimization and maximizing orders per delivery run, Asian food delivery platforms may have a much better shot at improving margins.

The data in this Bloomberg article offers more clues.

The math, and Meituan’s potential, can be dizzying. China’s urban areas have 2,426 people per square kilometer (6,283 per square mile), almost eight times the comparable U.S. population density. While the U.S. has 10 cities with 1 million or more people, China has 156. Deliveries in China cost about $1, compared with $5 in the U.S., iResearch says. Meituan retained about 63 percent of the country’s meal delivery market at the end of 2018, according to Bernstein Research, even as Alibaba spent billions over the previous several years to capture most of the rest.

These advantages translate to the rest of Asia as well.

- India and SE Asia also have large cities with high population density.

- Parking regulations are not stringently followed (and may often not exist) – which leads to a lower turnaround time per delivery on a multi-delivery route.

- Lower wages – especially as most delivery agents migrate from Tier 2 towns with lower income levels – improve the economics further.

Margin attacks: What’s good for the platform is bad for the ecosystem

With ever-thinner margins, split three ways between platform, delivery agent, and restaurants, food delivery platforms have been looking at new ways to ‘eat into’ the margin of their other stakeholders.

Option #1: Eat into the delivery agent’s share of the pie

Delivery platforms, in general, control the delivery price and payout policies, with no control for the delivery agent. As a result, one way to eat into more margin is to reprice deliveries or to change delivery incentives in a manner that maximizes the margin for the platform, often at a cost to the delivery agent. I’ve written extensively about that in my work with the International Labor Organization (ILO) (Refer: Section 7.4). An extract below:

During its initial launch, UberEats offered workers £20 per hour. As consumer demand grew and the platform gathered momentum, its workers began to depend on this level of income. Then the platform implemented a more complex incentive formula involving £3.30 per delivery plus £1 per mile plus a £5 “trip reward”, subject to a 25 per cent transaction cut levied by Uber. A subsequent policy change revised the trip reward to £4 for weekday lunches and weekend dinners, and to £3 for weekday dinners and weekend lunches. Any delivery outside these periods didn’t earn a trip reward. Similarly, Deliveroo initially launched with an hourly wage mechanism in London, whereby couriers were paid £7 an hour plus £1 per delivery, plus tips and petrol cost; pay was subsequently reduced to a flat fee of £3.75 per delivery.

Option #2: Eat into the restaurant’s share of the pie

A far more effective (though disingenuous) approach is to ‘negotiate’ the overall margin with the restaurant. Here’s how this works:

Food delivery platforms offer marketing and delivery logistics. Platforms like GrubHub charge partly for their marketing services – aiding discovery of a restaurant – and partly for their delivery services – operating the delivery logistics for the restaurant.

When a customer discovers a restaurant on the platform and orders food, the restaurant is charged for both marketing and delivery. However, when a customer orders food from the restaurant’s website, using GrubHub delivery, the restaurant is only charged the delivery fee.

The marketing fee is a lot more attractive as it’s 100% margin, not split any further.

This is where things get interesting. Platforms like GrubHub now get into competing with top performing restaurants on Google Search.

Shivane believes GrubHub purchased her restaurant’s web domain to prevent her from building her own online presence. She also believes the company may have had a special interest in owning her name because she processes a high volume of orders. She rattles off a list of names of local restaurants that she suspects may be in the same predicament. I find versions of about half those names on the list of GrubHub-purchased domains. Additionally, it appears GrubHub has set up several generic, templated pages that look like real restaurant websites but in fact link only to GrubHub. These pages also display phone numbers that GrubHub controls. The calls are forwarded to the restaurant, but the platform records each one and charges the restaurant a commission fee for every order, according to testimony from GrubHub executives at a hearing at New York City Hall on Thursday. This happens on the GrubHub platform itself, too. The phone numbers you see displayed in the app typically aren’t a restaurant’s actual phone number, they’re the numbers that GrubHub uses to make sure it’s getting its commission.

This is essentially a ‘platform-as-producer’ play where the platform now directly competes with producers in its ecosystem. Unlike Amazon, which gets into retailing, GrubHub doesn’t get into the restaurant business, it only creates an ‘online illusion’.

This leads to an important question:

If a customer Googles a restaurant’s name and lands on a GrubHub-purchased site that looks like a real restaurant’s site, who should get the commission? And is it fair if GrubHub can outrank its own restaurants on search engines? “Buying the URLs and positioning yourself in that way so that even in transactions in which the customer would want to go straight to the business, or the business has the opportunity to compete, to have a direct relationship with the customer—it’s predatory to do that,”

Food delivery is growing rapidly but most players are unlikely to be pure intermediaries.

Feel Free to Share

Download

Our Insights Pack!

- Get more insights into how companies apply platform strategies

- Get early access to implementation criteria

- Get the latest on macro trends and practical frameworks

Beyond margin: The low risk, high return engine

We’ve looked at improving margin through greater demand-side integration. The other way to do this is through greater supply-side integration.

This is where ‘dark kitchens’ (or ‘‘cloud kitchens’ or ‘virtual restaurants’) come in. Without going into the nuances of the individual definitions, we’ll use this term to refer to cooking and food processing operations that are set up exclusively for delivery, and do not have a front-end restaurant interface. This video below provides a good introduction.

Most delivery platforms, at scale, start vertically integrating into ‘dark kitchens’.

U.K.-based food delivery giant Deliveroo, which counts Amazon as a major investor, recently revealed that it now claims 2,000 virtual restaurant brands in the U.K. alone — a 150% increase on the previous year. Deliveroo has operated delivery-only kitchens, called “editions,” since 2017.

Uber cofounder and former CEO Travis Kalanick has launched a new venture called CloudKitchens, which touts itself as a real estate company that provides “smart kitchens” for delivery-only restaurants. Last month, it closed a $400 million funding round at a reported $5 billion valuation.

Dark kitchens, in themselves, are a supply-side play. When combined with market-wide demand aggregation of a delivery platform, they can potentially out-compete most restaurants, on account of superior economics.

Netflix, but for food

The ‘delivery platform + dark kitchen’ integration playbook essentially works out as follows:

- Aggregate consumer demand and delivery logistics as a delivery platform.

- Partner with restaurants, build network effects, and learn from market-wide data to identify popular dishes, ordering patterns etc.

- Create a dark kitchen based on this data and optimise cooking operations around demand patterns.

Step 2 is critical. F&B is a high risk business. Individual restaurant owners take the risk of starting new businesses. They pay high rents for premium real estate. Delivery platforms learn from the risk taken across the ecosystem and build stronger demand models than any individual restaurant could.

This is a bit like Netflix sourcing content from production houses, serving demand at scale, learning from those demand patterns, and getting into content production itself. Except that it’s a lot simpler with food.

‘Dark kitchen’ economics

‘Dark kitchens’ benefit from:

- Lower real estate cost

- Lower cost of waste, a significant cost driver in F&B, as market-wide demand patterns can help predict sourcing and preparation

- Lower delivery costs as kitchens and delivery hubs can be located closer to demand, enabling superior route optimization. Cooking and sourcing can also be apportioned across locations based on demand patterns near those locations.

- The demand-side network effect could lead to supply-side scale in kitchen operations as more dark kitchens are set up. This enables centralized procurement across ‘dark kitchens’ improving margins further.

- Further improvements in margin with kitchen automation.

Overall, ‘dark kitchens’ allow delivery platforms to learn risk-free from their ecosystem partner restaurants – which individually take business risk – and enable them to create a higher margin business than all participant restaurants.

The road ahead… COVID-19 and a bear market?

Food delivery is growing rapidly but most players are unlikely to be pure intermediaries. As evidenced above, most of them will ‘eat into’ profitable positions on the demand side (and claim ‘marketing fees’) and/or the supply side (with ‘dark kitchens’). Venture capital subsidizes entry into both positions by first subsidising demand aggregation and then subsidising supply-side scale. At scale, and with improved margins, the model may start paying back.

The next several months are going to be interesting. GrubHub is likely up for sale. Antitrust investigations are on for the Amazon-Deliveroo merger. Growth capital will dry up further as the industry moves to consolidation. And the need for social distancing will require delivery companies to rethink delivery without human contact.

State of the Platform Revolution

The State of the Platform Revolution report covers the key themes in the platform economy in the aftermath of the Covid-19 pandemic.

This annual report, based on Sangeet’s international best-selling book Platform Revolution, highlights the key themes shaping the future of value creation and power structures in the platform economy.

Themes covered in this report have been presented at multiple Fortune 500 board meetings, C-level conclaves, international summits, and policy roundtables.

Subscribe to Our Newsletter