Strategy

The emerging financial services value stack

Rebundling finance – the key to success of fintechs in the platform economy

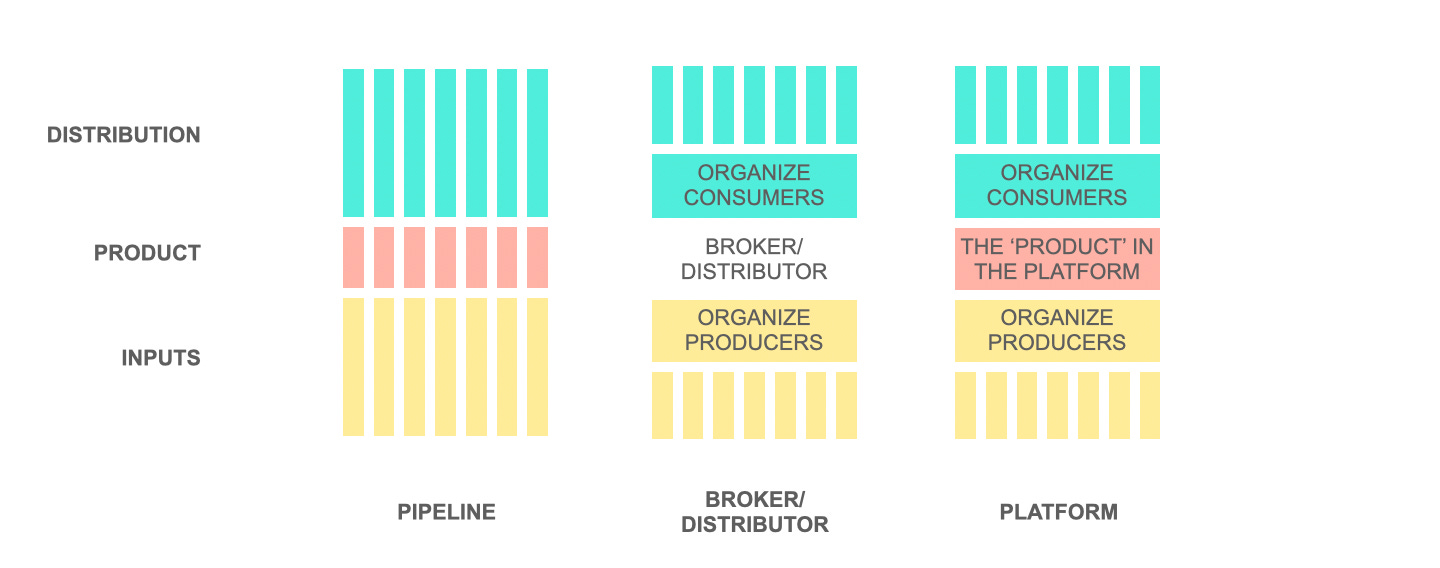

One of the emerging themes of the platform economy is the shift from vertically integrated value chains to horizontally layered value stacks.

This is happening across industries but the financial services industry provides a great template of how to think about this shift. This edition of the newsletter conducts a deep-dive on this topic.

One of the most frequently asked questions we answer for companies relates to helping them understand their strategy in a world of horizontally layered ecosystems. A couple of months back, I co-authored a whitepaper with Standard Bank, which lays out this shift for the financial services industry. This newsletter carries an overview of the key points from that analysis. You can also access the full whitepaper at this link.

Let’s dive right in…

From vertical to horizontal

Banks have primarily performed the transformation function and served to collect deposits and pay interest on savings. Other core functions included payments, lending, and asset management. Through the 1990s and early 2000s, banks bundled financial services and acted as ‘one-stop shops’ for their customers. However, these bundled services were not structured around customer needs – they were optimised around the capabilities of a bank’s delivery channel.

As transaction costs fall with the emergence of new digital infrastructures and new mechanisms to organise the market for financial services, the vertically integrated value chain starts to unbundle. This is giving rise to new specialised competitors – agile and innovative ‘fintechs’ that focus on specific tasks in the value chain.

From the late 2000s to the mid-2010s, we saw the emergence of fintech challengers that specialise in particular activities across the financial services value chain. In doing so, they effectively ‘unbundle the bank’. Venmo and Square started by specialising in peer-to-peer (P2P) payments, Mint specialised in budgeting, and Lending Club helped consumers identify P2P loans with the best interest rates.

This unbundling of the vertically integrated industry architecture is creating a more modular, layered ecosystem where firms at every layer specialise in a particular value-creating activity.

Multiple competing firms can take up positions that were previously occupied by a single financial services firm, thus driving down margins and expanding consumer choice.

In these modular ecosystems, firms increasingly retain those activities where they possess superior capabilities. Over time, this has a positive reinforcement effect, as these firms increasingly develop competitive advantages by specialising in their niches, while letting go of activities in which they are less strong. Moreover, the low costs of API-based coordination with other firms further validates specialisation, since firms can invest in specific capabilities in a particular part of the value chain, while participating in larger business ecosystems that consist of firms across layers.

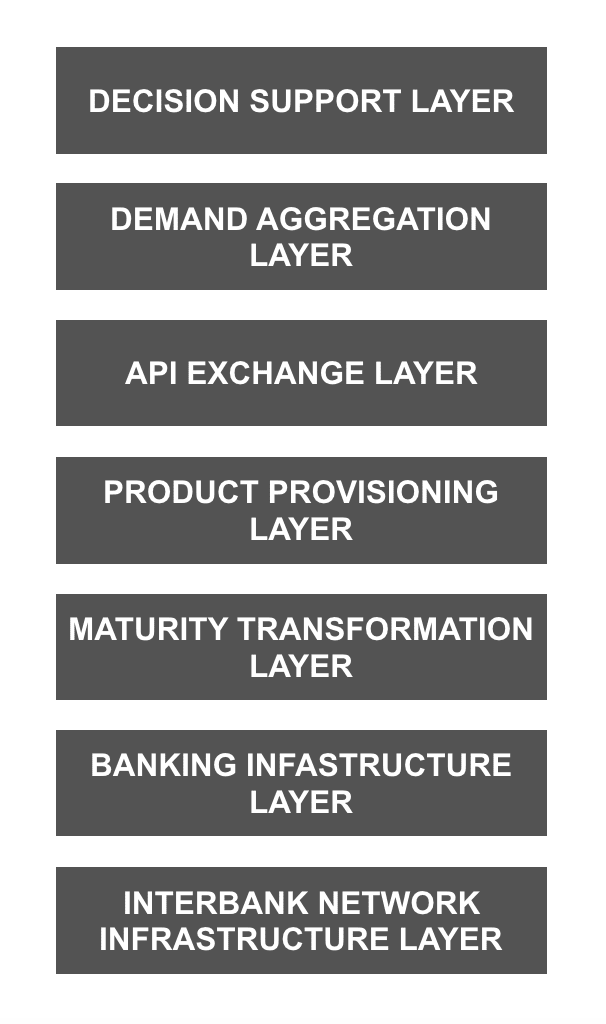

The emerging financial services stack

As the financial services industry reconfigures into ecosystems, and as value is directed towards new business models, the vertically integrated value chain of the financial services industry is being transformed into a layered financial services stack.

This stack has seven distinct layers that span the production and consumption ecosystems. The production ecosystem, further down the stack, comprises the underlying interbank network infrastructure, banking infrastructure, transformation functions, and product provisioning. Further up the stack, the consumption ecosystem spans consumer-focused decision-support systems and market aggregation platforms. Industry-wide integration infrastructures may play a role in the middle, linking the production and consumption ecosystems. We explore each layer in more detail below.

Value stack for your industry

This post lays out some of the core principles of value stack analysis.

If you’d like to learn more about our work here, check out our Advisory page or request our Advisory kit to get more details on our analysis and approach.

Interbank network infrastructure layer

Interbank network infrastructure provides direct links for banks to interact, enabling faster and secure communication and money transfer between banks on the same network.

The SWIFT payments network – and competitors like the Depository Trust & Clearing Corporation (DTCC) – provide clearing and settlement services to financial institutions.

Increasingly, distributed ledger technologies (DLT), like the Blockchain, enable more efficient record keeping for loans, investments, and even securities clearing. RippleNet, for instance, provides a DLT-based decentralized network for real-time settlement of international payments.

Inter-bank networks also include DLT-based trade finance infrastructure like Vakt and Contour. Multiple banks, often operating in consortia which include logistics and procurement companies, use a shared DLT-based infrastructure to seamlessly share documentation related to trade finance transactions.

Banking infrastructure layer

The banking infrastructure layer has traditionally been dominated by suppliers of core banking systems.

The monolithic technical architecture of traditional core banking systems discourages the modularity needed to participate in ecosystems. However, several firms, including Plaid, Tink, and TrueLayer, now enable banks to modularize banking products and services, making them accessible to external applications.

These firms open up core systems in corporate and retail banking as well as in treasury and capital markets through open APIs, allowing financial institutions to provision their products and services modularly and make them externally consumable as APIs on which external fintechs may develop new solutions.

Credit scoring is a key capability in the platform economy. Credit scoring enables access to credit, but can also serve as reputation scoring to determine access to other non-financial services.

While traditional credit access was collateral-based, emerging credit scoring models leverage other data sources. In the agricultural sector, Apollo Agriculture uses satellite imagery data to determine credit worthiness of farmers while APA Insurance uses similar data sets to inform risk. Companies like SyeComp gather geospatial data through a combination of satellite and drone based imagery. FarmDrive employs a blend of social, agronomic, environmental and satellite data to develop credit scores for farmers.

These capabilities, while traditionally bundled inside the bank, will increasingly be provided by independent firms. These firms, if successful, will provide these capabilities across multiple banks and learn from the data captured across activities across banks, further reinforcing their capabilities. In this manner, a bank’s ability to lend in the future will no longer be limited by its access to past lending and repayment data.

Improvements in AI can help banks forecast customer demand and internal liquidity needs better, eventually contributing to more effective transformation functions.

Feel Free to Share

Download

Our Insights Pack!

- Get more insights into how companies apply platform strategies

- Get early access to implementation criteria

- Get the latest on macro trends and practical frameworks

Maturity transformation layer

Maturity transformation lies at the core of a bank’s business, where it manages how depositors’ money may be used most effectively while also managing liquidity for the depositor to withdraw money as and when required.

Improvements in AI can help banks forecast customer demand and internal liquidity needs better, eventually contributing to more effective transformation functions.

Despite banks’ perceived advantages at this layer, the emergence of digital currencies – for instance, in China – poses potential challenges to banks’ ability to compete at this layer in the long term. The shift to digital currencies will quite likely erode retail deposits, as funds held in banks will be converted into crypto and will not be available to support lending. To sustain and grow the lending business, banks will need to look to move expensive sources of funds, including wholesale financing and/or debt issuance.

Product provisioning layer

Leveraging the three underlying layers, banks – as well as non-banking players that operate exclusively at this layer – create and provision financial products and services. With the shift to a platform economy, these products and services are increasingly consumable as APIs.

Products like loans and mortgages may be served as APIs but risk getting commoditized as open banking proliferates and offerings from multiple banks compete for the same customer’s attention.

On the other hand, some banking capabilities may even be deployed as key capabilities to enable interactions in third party platforms’ ecosystems. Stripe, one of the best examples of such a capability, allows developers to process payments and money transfers between customer and merchant accounts. In particular, noting the rising complexity of managing payments on multi-sided platforms, Stripe positioned itself as a payments enabler for the platform economy, managing collection across customer accounts and settlements across merchant accounts.

The ability to modularize and provision financial services as APIs enables unbundling and rebundling in the financial services industry. This rebundling typically occurs at one of the top three layers of the stack, in the consumption ecosystem, which we visit next.

The API exchange layer

The API exchange layer manages interactions across the production and consumption ecosystems of the financial services stack. On one hand, this layer aggregates product provisioning APIs across the financial services production ecosystem. On the other hand, it integrates across websites, apps, and other digital services in the consumption ecosystem, providing them access to these APIs.

In this manner, the API exchange layer is the first layer at which financial services may eventually be rebundled. A player at the API exchange layer may rebundle multiple third party financial services and resell the resultant solution to demand-side players further up the financial services stack.

The Plaid Exchange is an example of a player operating at this layer, and integrating this position back to its position at the banking infrastructure layer. Plaid Exchange enables banks to set up an integration and exchange layer around their products and data, allowing external data aggregators or fintechs to access these products and data.

With every bank provisioning its product as APIs, players at the API exchange layer manage the aggregation and provisioning of these APIs across multiple banks. Players at this layer also use core banking capabilities to make these APIs consumable by third-party non-banking entities.

The demand aggregation layer

Banks continue to be asset managers in the production ecosystem, but profit pools are increasingly shifting to platforms that own the customer relationship and data in the consumption ecosystem. In that context, the demand aggregation layer may well be the most powerful position across the entire financial services stack.

There are two distinct factors that create opportunity for players at the demand aggregation layer. First, the financial identity of the typical user is increasingly not owned by a traditional bank. One of the biggest opportunities for banks and asset managers is to rethink their business models to best own and curate the financial identity of the user. Second, the ability to aggregate demand is increasingly shifting from players that serve secondary demand to those that serve primary demand. For example, a car purchase is a user’s primary demand while the car loan is secondary to that. In the platform economy, firms will need to understand the user’s primary demand in order to own the secondary demand.

Insurance firms are, similarly, well positioned to play at the decision support layer. While insurance firms have data-driven business models, they traditionally captured data as a one-time event to determine a customer’s risk profile and price her premium. At the demand aggregation layer, insurance firms have the opportunity to move from this one-time data capture event to a continuous data flow, leveraging connected devices and digital services, which build up this data flow. Some insurers like Progressive Insurance provide data-capturing devices for cars to capture driving behavior and provide a personalized premium based on the data. These data flows can also inform product innovation at insurance firms.

More importantly, over time, insurance firms can bring in third parties on board to serve these users, based on this data. While insurance serves a secondary need arising out of an adverse event, these third parties can serve the user’s primary needs. For example, data captured on a user’s wellness or driving habits may be used to build platforms that serve services from third parties. Health insurers can build platforms that connect patients with wellness and care services. Auto insurers can, likewise, serve value-added services from driving schools, service centers, fuel stations, and so on,

Financial profile aggregators, like Mint and Yolt, aggregate data across financial institutions to create a single financial profile for the user and serve unified analytics to the user. These aggregators also connect users with relevant offers from third parties. In general, countries with a fragmented banking landscape with multiple financial relationships per user are most likely to support this model. However, with widespread API deployment, the barriers to entry for such a business model go down. The competitive advantage for financial profile aggregators was based on their proprietary screen-scraping technologies. As banks open up APIs, data aggregation is less of a challenge. In this new scenario, these platforms will need new data beyond bank account data to differentiate themselves and will also need to get third parties on board faster, in order to provide many more relevant services to the user, beyond financial services.

Peer-to-peer marketplaces for financial services also aggregate demand at this layer. Where traditional banks do not lend without collateral, peer to peer lending platforms facilitate entirely new interactions using alternate sources of data that banks typically do not have access to or do not use. On the other hand, as lending platforms gather more data about their ecosystem, manual curation and underwriting can increasingly be taken up by algorithms, which scales the underwriting process. As more diverse data comes in, the platform’s ability to predict high quality borrowers increases, which in turn leads to lower risk. As the risk goes down, the platform can price loans more attractively, leading to even more lending activity and more data. This creates a positive feedback loop.

The decision support layer

The final layer at the top of the stack is the layer at which the consumer chooses and consumes a financial service. Decision support to this choice is the primary value driver at this layer.

If bank branches were the demand aggregation points in the traditional financial services value chain, the advisors, agents, relationship managers, and salespeople formed the decision support layer.

However, with improvements in AI and natural language processing, new data-driven decision support systems can be deployed to inform and aid the user’s purchase and consumption decisions. AI-enabled chatbots and robo-advisory enable scalable and customized deployment of the decision support function to consumers. In general, firms that have unique access to data flows and scoring mechanisms will be best positioned to enable decision support in the platform economy.

More importantly, the decision support layer requires banks to move beyond banking. If banks are to occupy a central position in their respective ecosystems, they will need to address customers’ financial needs in the context of the non-financial need that drives demand for the financial need. Banks and insurers will need to move from serving the secondary demand through a loan or insurance product to serving the primary demand, in order to compete effectively at this layer. Banks and insurers which can understand and own the primary demand of the user – around buying a home or buying a car – will be best positioned to differentiate and gain profits even as the traditional lending and insurance businesses themselves get commoditized. For instance, mortgage providers will need to understand the overall customer journey across house search, purchase, ownership, and sale. Similarly, payment providers will need to understand consumption preferences to better serve their customers at the point of need and retain primacy of decision support. As banks and insurers participate in the primary demand, they will be better positioned to monetize non-financial interactions.

Strategy for the platform economy

The stack provides a central framework for strategy development in the platform economy. As we note with the examples above, banks may take up different positions across the stack to configure their business models.

Banks will have to engage in strategy development in a three step framework:

- First, banks will need to selectively determine which positions in the value stack they continue to play in and which businesses they divest

- Second, having chosen positions across the stack, they will need to reinforce across these positions by developing business models that integrate multiple positions

- Finally, banks will need to develop a mechanism to monitor competitors, especially indirect competitors who move into their position from another layer of the stack

Choosing positions across the stack

To develop competitive advantage in the platform economy, financial institutions cannot rely on traditional vertical integration. Instead, they will need to strategize across the stack. Banks that merely follow the herd into open banking, without making strategic choices across the stack will rapidly see themselves getting commoditized. Those that do not migrate from serving secondary demand to serving primary demand will face growing challenges in the consumption ecosystem as non-banking players wrest consumer engagement away from traditional banks.

Banks will most likely continue to play a strong role at the maturity transformation layer and will continue to serve products at the product provisioning layer. However, these plays are unlikely to create competitive advantage in the platform economy as most of these banks become relegated to the position of commoditized producers in other platforms’ ecosystems. In order to compete effectively, banks will have to play at one or more of the three platform positions mentioned above. Alternatively, financial institutions with a strong technology play could develop capabilities to provision within other financial and non-financial ecosystems.

Integrating positions across the stack

Banks will need to strategize separately for each layer but will also have to think across the stack to integrate their advantages across multiple layers. For instance, banks that operate at the demand aggregation layer as well as the API exchange layer will compete more effectively at the API exchange layer because of their access to a proprietary source of demand. Similarly, banks that operate at the decision support layer and develop access to unique consumption data can use that data to better inform credit scoring in the production ecosystem. This, in turn, improves their ability to provide decision support in the consumption ecosystem, thereby creating mutual reinforcement across the positions.

Monitoring movements across the stack

Possibly the most interesting component of ecosystem competition is the lateral competition that emerges when companies in another layer of the value stack develop the capabilities to move into your layer of the value stack. Consider, for instance, a payment provider like Stripe moving into identity management of merchants and eventually into providing business setup services to those merchants. Or Ant Financial starting with Alipay at the demand aggregation layer and subsequently moving into the banking infrastructure layer with Caifuhao. Dominant platform ecosystems rarely operate at one single position on the stack. Instead, they migrate to new positions and by integrating across these positions, they are better able to compete against players who specialize at a particular layer of the stack. Hence, banks should proactively monitor for companies making movements across the stack.

Value stack analysis for platform ecosystems

Value stack analysis applies across industries. As businesses increasingly participate in ecosystems that span multiple industries, understanding value layers in those industries and strategizing across those value layers is critical. Over the past three years, we’ve done this increasingly across ecosystems as diverse as smart mobility, decentralized energy, logistics, construction, education, healthcare, and consumer goods.

If you’d like to learn more about our work here, check out our Advisory page or request our Advisory kit to get more details on our analysis and approach.

Previous article on Platform Economy Next article on Platform Economy

Previous article on Platform Economy Next article on Platform Economy

State of the Platform Revolution

The State of the Platform Revolution report covers the key themes in the platform economy in the aftermath of the Covid-19 pandemic.

This annual report, based on Sangeet’s international best-selling book Platform Revolution, highlights the key themes shaping the future of value creation and power structures in the platform economy.

Themes covered in this report have been presented at multiple Fortune 500 board meetings, C-level conclaves, international summits, and policy roundtables.

Subscribe to Our Newsletter