The Financial Services Playbook

The fast-growing platform economy, in which value-creating interactions are facilitated by digital intermediaries, presents financial services institutions with new opportunities to deepen their customer relationships and tap into non-traditional revenue streams. This paper explores how financial institutions can strategize and win in the platform economy.

CO-AUTHORED BY:

Four Key Highlights

Transformation into a Platform Business

Financial firms may choose to evolve into platform businesses themselves, enabling them to tap into new growth opportunities by connecting various stakeholders within their ecosystem.

Collective Action by Incumbent Firms

Incumbent financial firms may collaborate and engage in collective action to better meet customer needs. This collaborative approach can involve sharing resources and expertise to create more comprehensive and competitive offerings.

Development of Licensable Capabilities

Organizations in the financial sector can develop innovative capabilities and services that can be licensed or shared across ecosystems. This approach allows them to monetize their expertise and expand reach beyond their traditional boundaries.

Continued Product Provider Scale

Financial companies may opt to focus on building scale as product providers, emphasizing the expansion of their core offerings to maintain their competitive position and attract a larger customer base.

Key Insights of Ecosystem Innovation

The Rise Of The Platform Economy

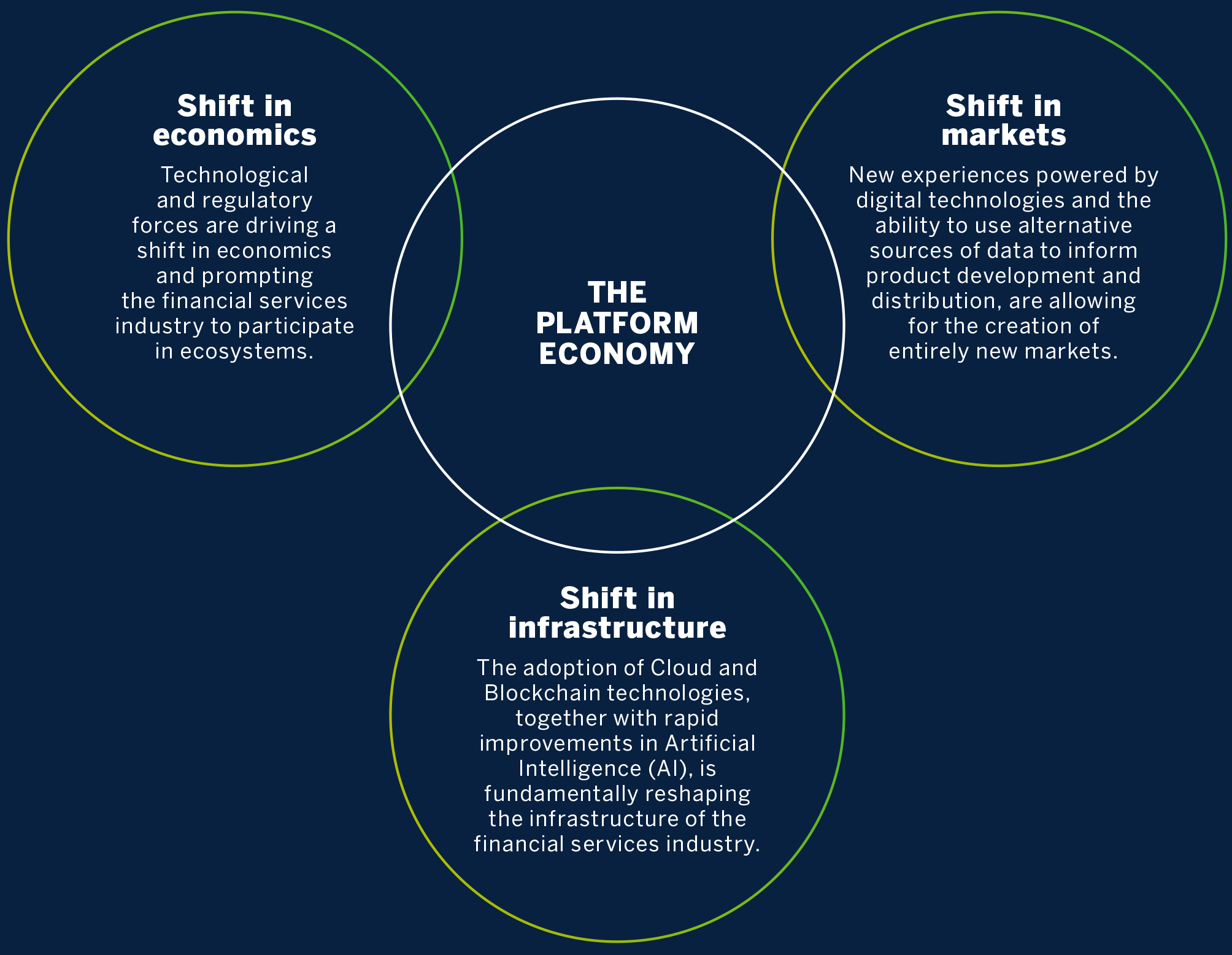

The platform economy’s rise is being powered by a shift in industry economics, in market behaviors, and in infrastructural technologies. There are 3 key shifts playing out and impacting the traditional financial services value chain.

Technological and regulatory forces are driving a shift in economics and prompting the financial services industry to participate in ecosystems.

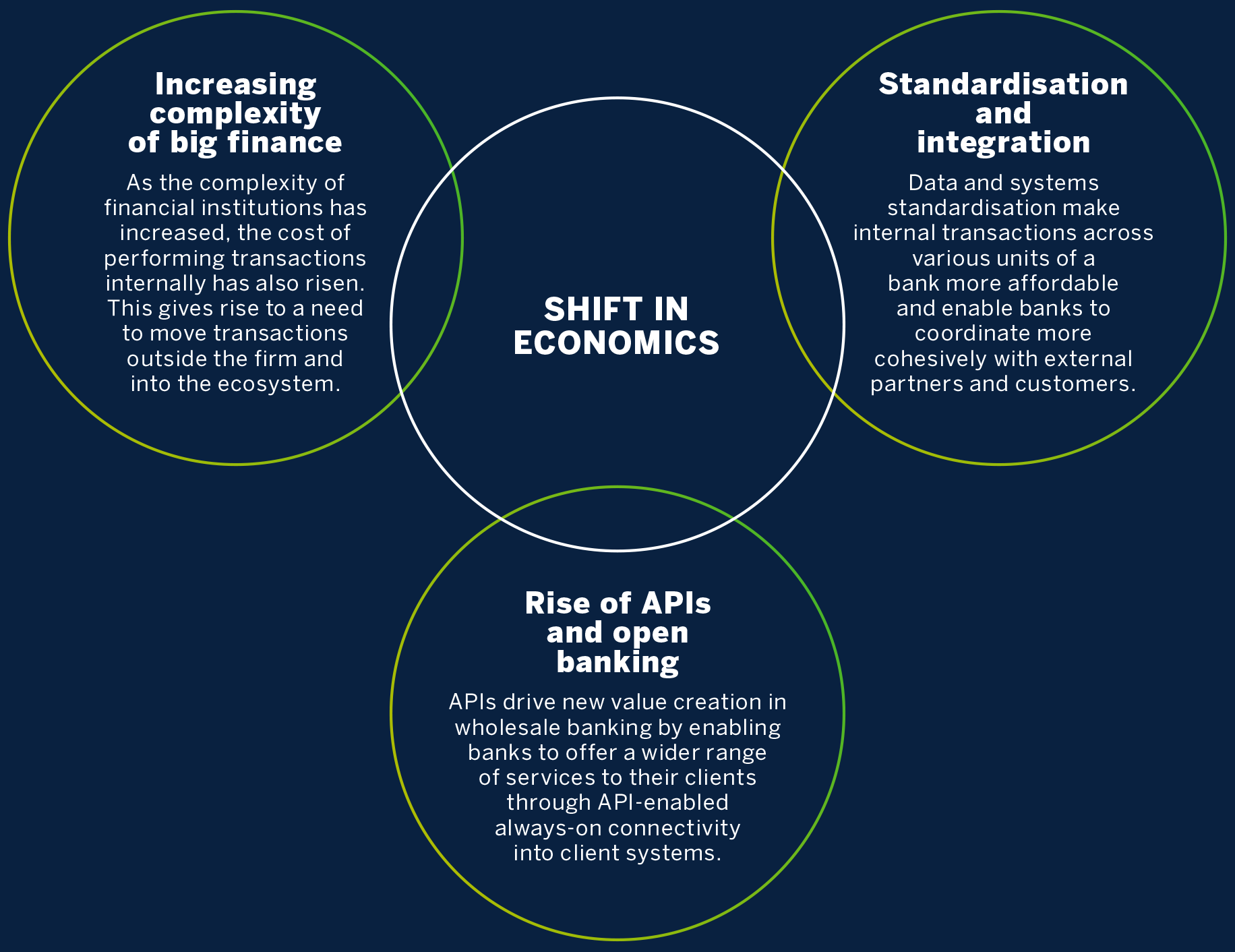

Increasing complexity is pushing the industry into modular ecosystems

Complexity and cost of internal transactions within financial institutions has increased. This, in turn, has pushed the financial industry into modular ecosystems and gives rise to a need to move transactions into an ecosystem environment.

Several factors have driven this increasing complexity. A greater focus on regulatory compliance following the global financial crisis has led to increased data collection, monitoring, and reporting costs, particularly in large, complex operations.

Standardization and integration make internal transactions cheaper

Advancements in cloud computing and data management technologies have allowed financial institutions to standardize their internal data and processes. This streamlines workflows, enables centralized data management, and enhances the ability to derive value from data. Internal standardization also automates compliance and regulatory reporting, improves loan profitability, reduces default risk, aids in monitoring financial crime, and enhances debt collection efficiency. Ultimately, it makes internal transactions more cost-effective and fosters better coordination with external partners and customers within banks.

APIs and open banking

The financial services industry is undergoing significant changes due to the rise of application programming interfaces (APIs) and cloud-hosted workflows.

APIs drive new value creation in wholesale banking by enabling banks to offer a wider range of services to their clients through API-enabled always-on connectivity into client systems.

While internal standardization streamlines operations, APIs reduce external transaction costs, leading to a shift from traditional vertical integration to business ecosystems.

APIs enable seamless coordination between internal processes and external parties, enhancing flexibility and product distribution. Regulatory forces, like Europe’s PSD2, are pushing for open banking, allowing external players to participate. Such trends may facilitate financial inclusion.

APIs drive value creation in wholesale banking by expanding service offerings and improving connectivity.

Emergence of New Markets

New experiences powered by digital technologies and the ability to use alternative sources of data to inform product development and distribution, are allowing for the creation of entirely new markets.

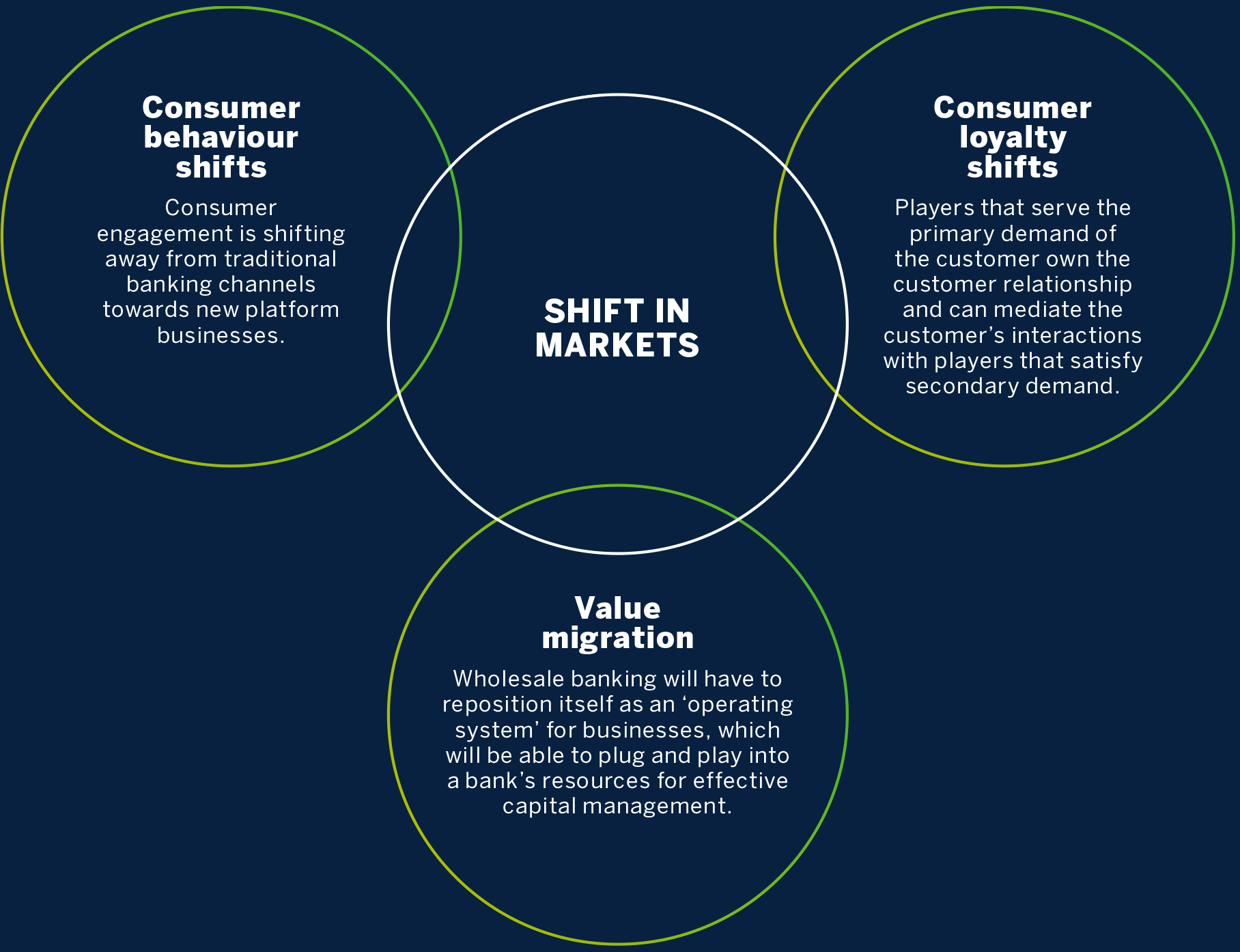

Pandemic-induced behavioral shifts and the value chain

The pandemic has led to significant behavioral shifts and the reconfiguration of business landscapes. This has resulted in the migration of value from established positions to new opportunities, often driven by innovative business models.

The crisis accelerated the adoption of contactless payments in the financial services industry, solving previous adoption challenges (chicken-and-egg-problem) and paved the way for new payment ecosystems, new value pools and value creation at scale.

Contactless payments essentially unbundled payments initiation and acceptance from physical cards and terminals – functions that can now be embedded into any interface or devices that can engage in machine-to-machine payments.

Shift in consumer loyalty : From product owners to experience curators

Digital platforms have disintermediated the traditional relationships between financial service firms and customers. These platforms own the consumer relationship in serving primary customer demands (e.g., housing or mobility)

To stay competitive, financial institutions, including banks and insurers, must shift their focus and reposition themselves as an ‘Operating System’ that can easily plug and play into a bank’s resources to address primary customer demands and expand their services, in this changing landscape.

Modularity in Financial Services

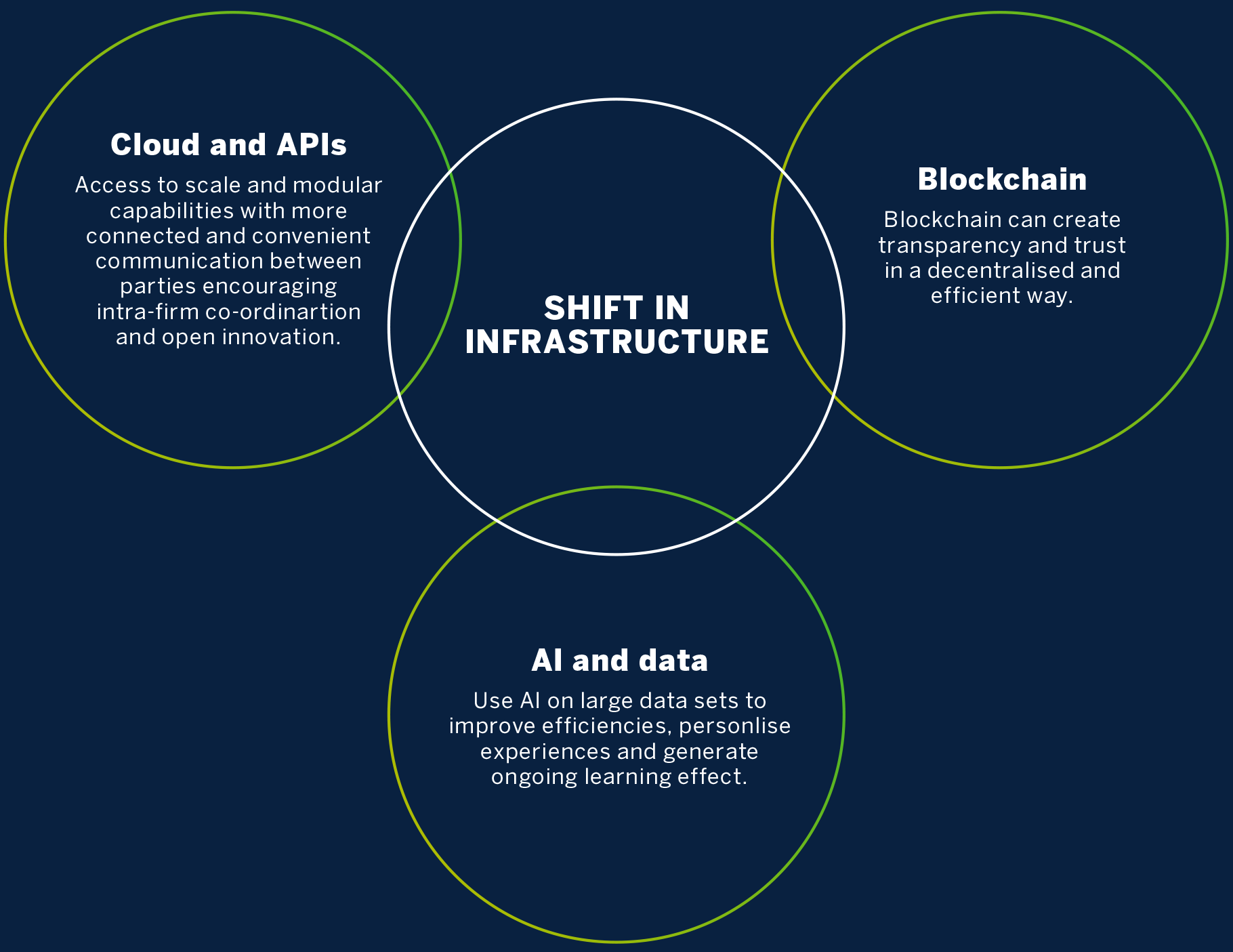

The underlying infrastructure of the financial services industry is being fundamentally reshaped by the adoption of cloud, blockchain, and AI technologies. A platform business model provides open infrastructure for these interactions and sets governance conditions for them.

The shift to platforms is making financial services more modular, efficient, and personalized and is also creating new opportunities for intra-firm coordination and open innovation.

Key technologies that are driving the shift in financial services industry

- Cloud: Cloud services are making financial services more modular and scalable. This allows firms to more easily and quickly deploy new products and services, and to respond to changing customer needs.

- APIs: APIs enable inter-firm communication and coordination, which can lead to open innovation and new products and services.

- Blockchain: Blockchain technology can address many of the challenges inherent in traditional centralized banking, such as transparency, trust, and efficiency.

- AI: AI can be used to automate high-volume transactions, personalize customer experiences, and build more sophisticated risk and credit models.

The Layered Ecosystem

The traditional vertically integrated value chains in the banking and financial services industry are evolving into horizontally layered ecosystems. This transformation is driven by the emergence of fintech companies specializing in specific tasks within the financial services value chain, effectively “unbundling the bank.”

This is being driven by the emergence of new digital infrastructures and mechanisms to organize the market for financial services, which have reduced transaction costs and made it easier for new firms to enter the market.

The unbundling of the industry is creating a more modular, layered ecosystem where firms at every layer specialize in a particular value-creating activity. This is driving down margins and expanding consumer choice.

From unbundling to ‘rebundling’

The financial services industry is undergoing a significant transformation, driven by the rebundling of financial services. While unbundling provides advantages, it also results in a fragmented customer experience and increased search costs. This evolution from unbundling to rebundling in the financial services industry is likely to continue, as unbundled services will likely serve as entry points to attract customer engagement and then rebundle services around consumer needs.

This transformation is being driven by a number of factors, including the need to improve the customer journey, reduce search costs for consumers, and create more sustainable business models.

Three-step process of rebundling in business ecosystems

- Gain primacy of the consumer relationship by offering an unbundled service.

- Leverage the customer relationship to capture data and build superior identity management and credit scoring capabilities.

- Use these capabilities to understand and predict customer needs, eligibility, and relevance, then rebundle other financial services around the consumer.

This approach allows firms to offer more personalized and relevant products and services to their customers, while also improving their own profitability.

Examples of rebundling in the financial services industry:

- Square: Expanded from a phone-based point-of-sale terminal for on-demand workers into a financial services platform focused on businesses’ financing, payroll, and payments needs.

- Ant: Started out as Alipay – a payments provider – and then added lending and other financial products.

- Stripe: Started as a payments API and now combines small business solutions and treasury services.

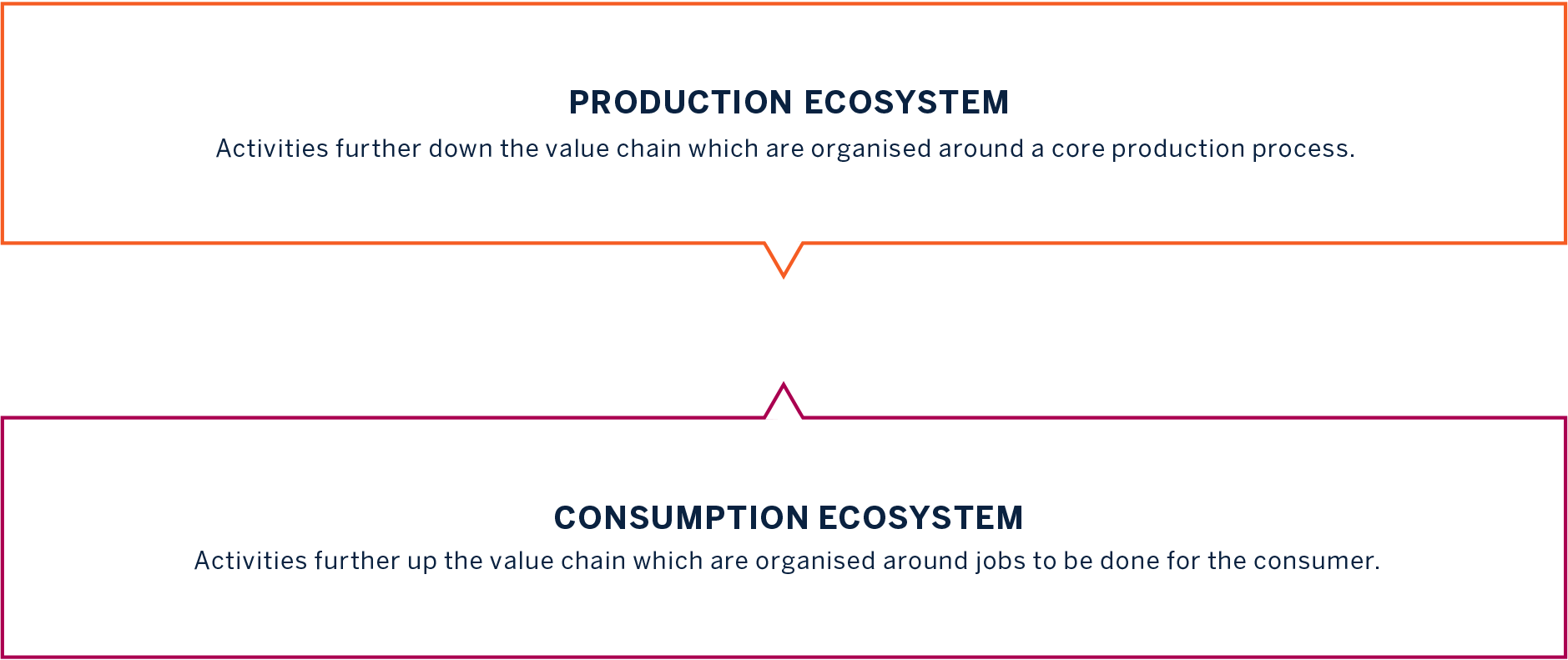

Production and consumption ecosystems

The financial services platform economy is transforming the way that financial services are produced and distributed. This transformation is creating new opportunities for firms and consumers alike. The decoupling within the financial services industry is happening because of the emergence of two distinct business ecosystems.

Production ecosystems

Business ecosystems that are organized around a core production process, such as fraud detection or risk assessment. These ecosystems rely on mechanisms to coordinate components across firms, such as common standards and APIs.

Consumption ecosystems

Business ecosystems that are organized around jobs to be done for the consumer, such as buying a home or saving for retirement. These ecosystems rely on mechanisms to reduce search costs for consumers, such as aggregation services and recommendation engines.

This decoupling is creating new opportunities for financial firms to specialize and collaborate, on the emergence of new products and services that are more tailored to the needs of consumers.

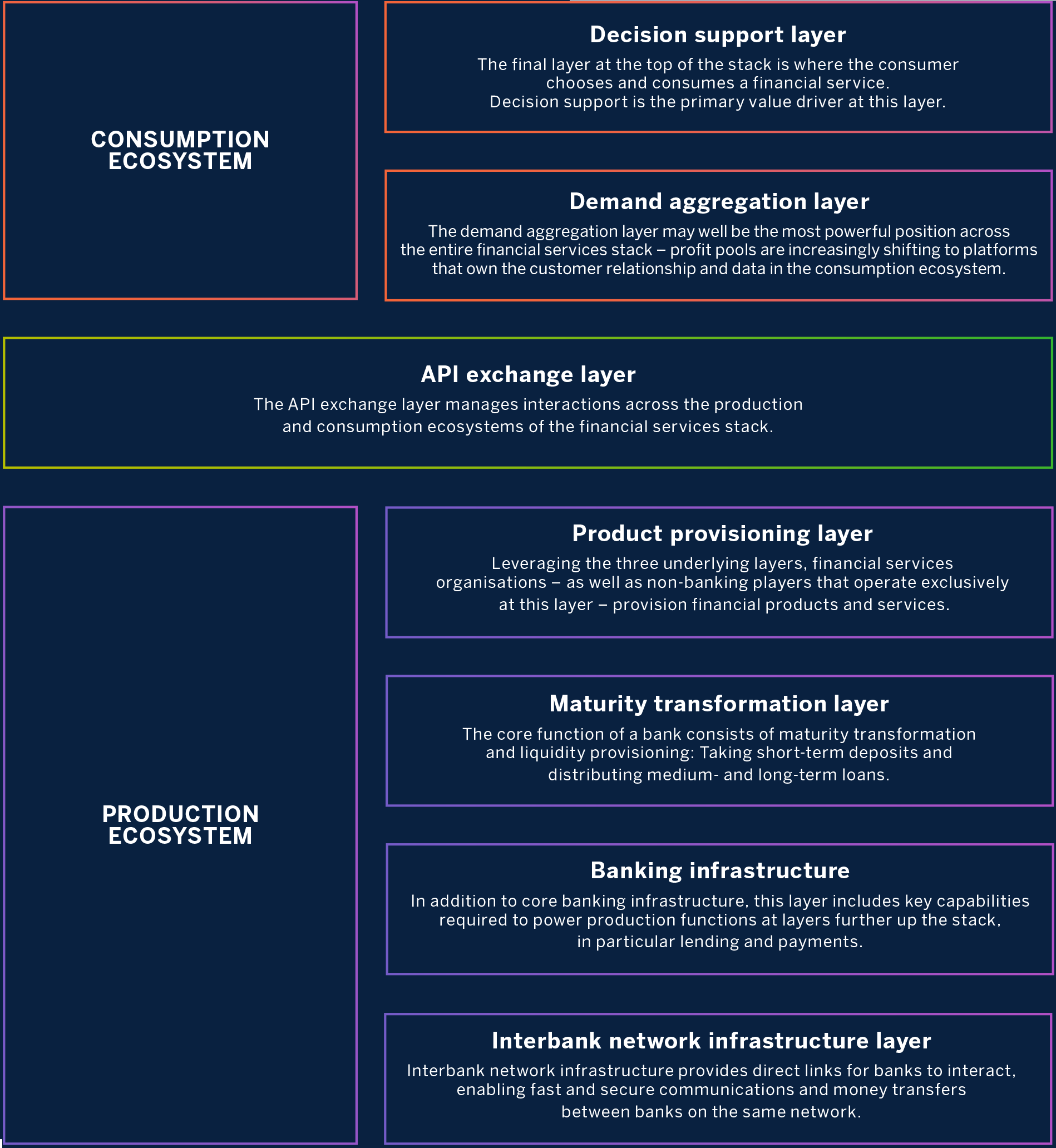

The Layered Financial Services Stack

The financial services industry is reconfiguring into ecosystems and shifting towards new business models, transforming the vertically integrated value chain into a layered financial services stack.

The stack has seven layers, with the production ecosystem at the bottom comprising underlying infrastructure, banking infrastructure, transformation functions, and product provisioning. The consumption ecosystem at the top spans consumer-focused decision-support systems and market aggregation platforms. Industry-wide integration infrastructures may link the two ecosystems.

Platforms play a key role in enabling collaboration and innovation and coordinating interactions in both the production and consumption ecosystems of the financial services stack.

However, platforms at different layers of the stack take on entirely different functions and architectures.

- At the demand aggregation and decision support layers, they aggregate consumer demand, control consumer data, and facilitate interactions with financial service providers. These platforms offer personalized experiences, benefiting from learning and network effects.

- At the API exchange layer, platforms manage distribution and financial service partners, promoting rebundling and expanding choice through network effects.

- In the production ecosystem, platforms provide core infrastructure, standards, and data assets, coordinating activities and attracting third-party providers. They foster interoperability, industry-wide data collection, and learning effects for improved prediction models and platform adoption.

By coordinating interactions between participants at different layers, platforms help to create more efficient and effective markets for financial services.

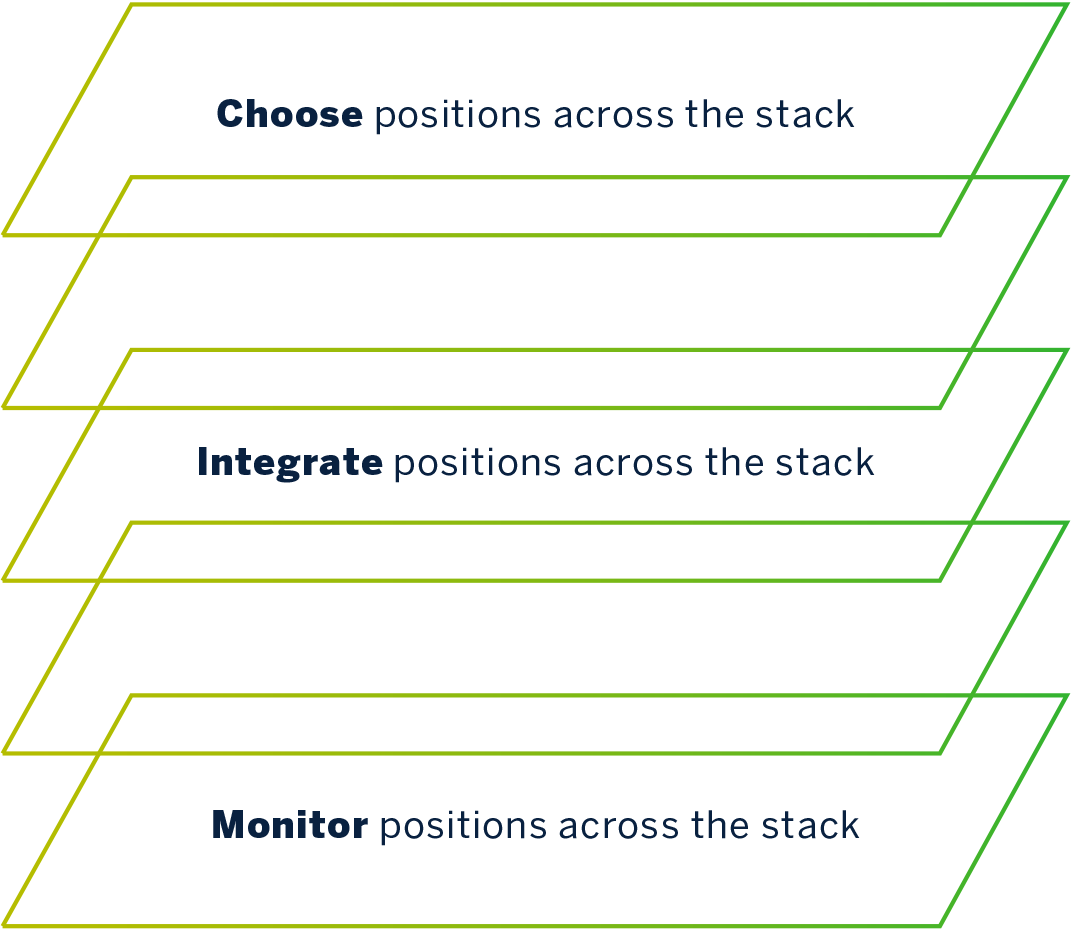

The Three Step Strategy Framework

Financial services firms will have to engage in strategy development in a three-step framework:

Choosing positions across the stack –They will need to selectively determine which positions in the value stack they will continue to play in, and which businesses they divest.

Integrating positions across the stack – Having chosen positions across the stack, they will need to reinforce these positions by developing business models that integrate multiple positions.

Monitoring movements across the stack – Firms will need to develop a mechanism to monitor competitors, especially indirect competitors who move into their positions from another layer of the stack.

In conclusion financial institutions must strategize across the stack to develop competitive advantages in the platform economy, or risk becoming commoditized and losing relevance.

Position in the New Financial Value Stack

Incumbent firms with product-based business models must adapt to the platform economy by taking up new positions on the value stack and defending existing ones, using a mix of offensive and defensive strategies.

This paper outlines four common types of strategies pursued by firms in the platform economy.

1.) Transforming into a platform business

Incumbent firms can transform into platform businesses by taking up positions in different layers of the stack, such as API exchange or demand aggregation.

Examples: Italian bank Banca Sella Spa’s Fabrick and Discovery’s Vitality platforms are two examples of how incumbent firms can transform into platform businesses to create new opportunities and competitive advantages.

By taking up positions in different layers of the stack, such as API exchange or demand aggregation, these firms have been able to expand their reach and customer base, offer new and innovative products and services, and generate new sources of revenue.

2.) Engaging in collective action in partnership with other incumbent firms

Collective action by incumbents can be an effective strategy to dominate a layer of the stack, level the playing field, or respond to platforms at scale.

The following examples show how incumbents can use collective action to maintain their competitive position in the platform economy. By working together, incumbents can pool their resources, share their expertise, and develop new solutions that would be difficult or impossible for them to achieve individually.

- New distributed ledger technologies: Multiple incumbent banks pooling their data resources to coordinate better without requiring central platforms.

- Shared services: Swish, a payments service launched by the top six banks in Sweden in cooperation with the central bank.

- Public-private partnerships: The India Stack, which provides underlying public digital infrastructure comprised of a biometric identity management system and e-KYC and e-documentation services, as well as an instant payments system that enables API-based peer-to-peer money transfers.

- Common datasets: Mozilla’s Common Voice project aggregates global voice data training sets to counter Amazon and Google’s control over speech recognition data.

3.) Developing capabilities that other platforms need

Financial services firms can build capabilities to play a critical role in other platforms’ ecosystems by offering KYC and credit scoring capabilities to third-party non-financial ecosystems. This is especially relevant in Africa, where the population remains largely unbanked.

4.) Defend existing value chain positions

Financial institutions can defend their existing value chain positions as producers by partnering with platforms to expand distribution and gain access to new clients, improve balance sheet management, and consume data flows to create new value. They should employ a combination of these strategies and time them well, as collective action needs to be coordinated before any single firm develops powerful network effects.

Map your

digital ecosystem strategy

- Leverage our extensive library of ecosystem maps created across different industries

- Determine potential value pools and business models in your industry

- Design and strategize for platform business models within the defined industry ecosystem

- Identify ecosystem control points to gain competitive advantage

Engage Our Advisory

Ecosystem Strategy and Business Model Design

Our most popular engagement model, offering multi-week remote and in-person expert advisory services to outline and design a platform business model and strategy

Learn More

Ecosystem Execution and Innovation

In partnership with a global consulting firm, we work with clients to drive their execution through a tried and tested platform execution process model.

Learn More

Ecosystem Education and Evangelism

Executive leadership learning programs and corporate-wide training program, based on the research behind international best-selling books, Platform Revolution and Platform Scale

Learn More

Download Our Advisory Kit

To discover how we can transform your platform business